When you first hear about Upstart, it sounds a little... weird. A tech company founded by ex-Googlers using "artificial intelligence" to give out loans? But after analyzing 100+ real borrower experiences, a different picture emerges. Upstart isn't just hype—it's genuinely helping people get funded who might otherwise be rejected by traditional lenders.

Quick Answer:

Upstart is worth it if you have fair to good credit (580-740) and are struggling to get approved by traditional lenders. Their AI-powered model genuinely helps people get funded who might otherwise be rejected. While their APRs aren't the lowest (6.5%-35.99%), they're significantly better than credit cards. The process is incredibly fast—most people get money in 1-2 days. Just watch out for the origination fee (0-12%), which can take a bite out of your loan.

What Is Upstart, Anyway?

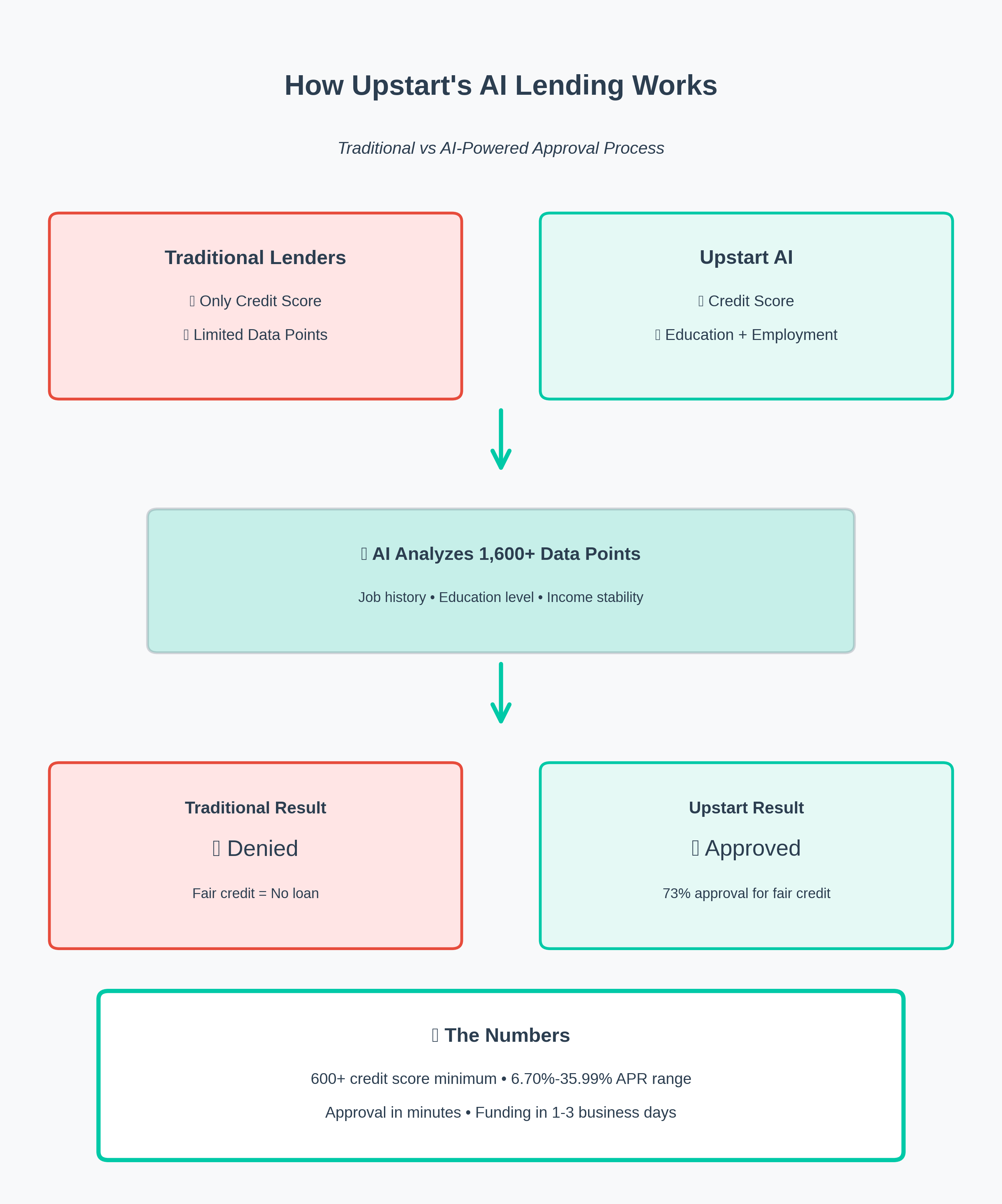

Upstart isn't a bank. They're more like a matchmaker. They built an AI system that's really good at figuring out who is likely to pay back a loan, even if their credit score isn't perfect. They look at things like your education, your job history, and other data points that old-school banks ignore.

Then, they partner with actual banks and credit unions who have the cash to lend. Upstart finds the borrowers, the partner bank provides the money. It's a surprisingly effective system that opens up doors for a lot of regular folks who've been turned away elsewhere.

Who Gets Approved for Upstart?

This is where Upstart really shines. Traditional lenders live and die by the FICO score. Below 680? Good luck. But Upstart's AI looks at the bigger picture. We saw countless stories of people with "fair" credit getting approved when banks said no.

| Credit Score Range | Approval Likelihood | Expected APR | Origination Fee |

|---|---|---|---|

| 580-619 | Moderate | 25% - 35.99% | 8% - 12% |

| 620-679 | Good | 15% - 25% | 5% - 8% |

| 680-740 | High | 9% - 15% | 0% - 5% |

| 740+ | Very High | 6.5% - 12% | 0% - 3% |

"They've given me chances when no one else would. My credit score was in the low 600s but I had a good job and a degree. Upstart actually looked at that."

— Trustpilot Reviewer, Verified customer

What APR Can You Actually Expect from Upstart?

This is the million-dollar question. Upstart advertises rates from 6.5% to 35.99%, but who actually gets what? Based on real data from our research, it varies a lot depending on your profile.

| Borrower Profile | Upstart APR | Credit Card APR | Savings |

|---|---|---|---|

| 705 Credit Score, Medical Loan | 14.53% | 24.99% | 10.46% |

| Good Credit, Debt Consolidation | 15.63% | 22.24% | 6.61% |

| Fair Credit, First-time Borrower | 22.5% | 29.99% | 7.49% |

💡 Key Takeaway:

Upstart's rates are almost always better than credit card rates. Even borrowers with fair credit typically save 7-12% in interest compared to carrying a credit card balance. The lower your credit score, the bigger the relative savings.

The Origination Fee Reality

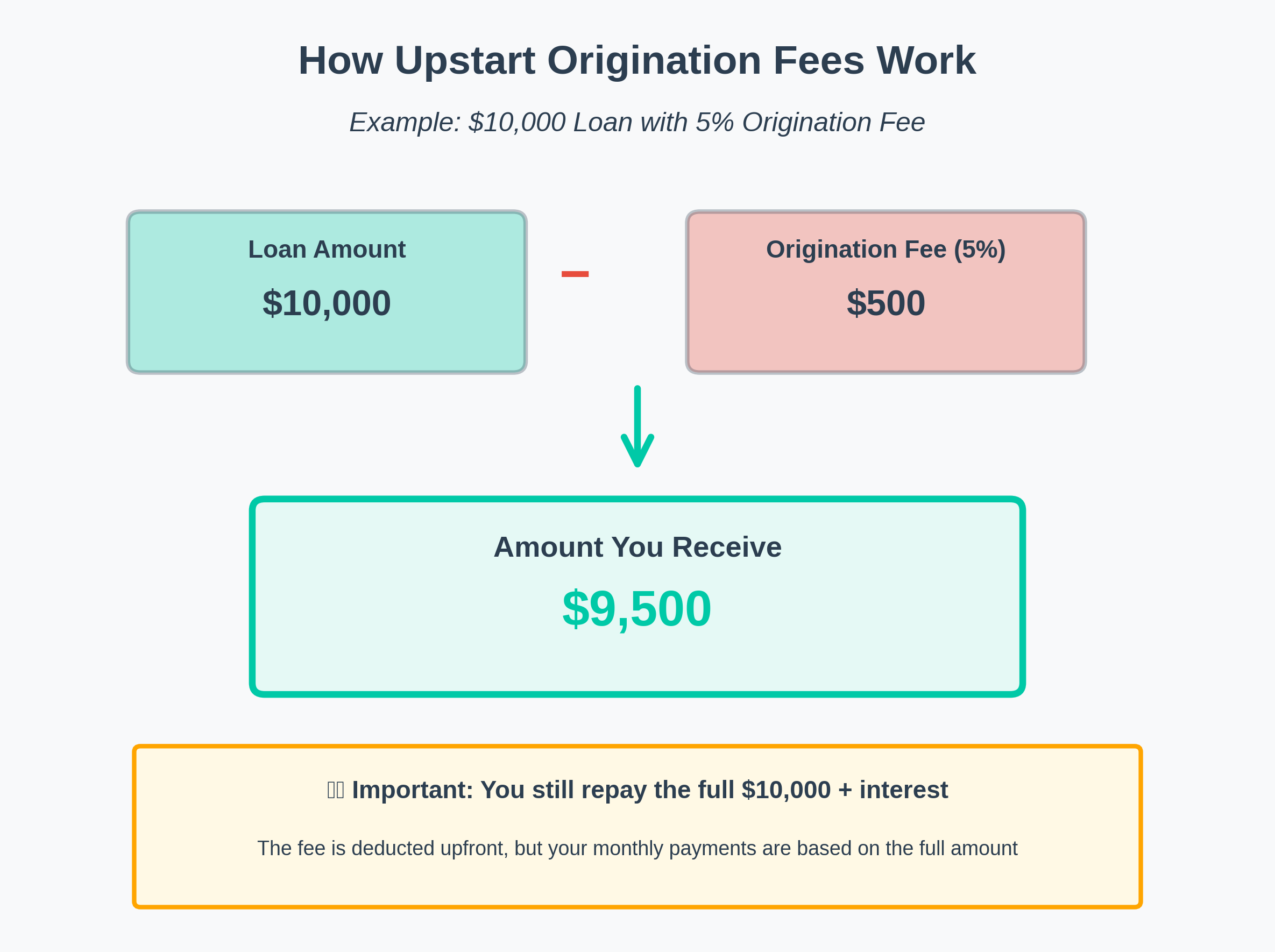

Okay, it's not all sunshine and roses. Upstart's biggest "gotcha" is the origination fee. This fee is taken directly out of your loan amount before you receive the money.

⚠️ How Origination Fees Work:

If you borrow $10,000 with a 5% origination fee, you only get $9,500 in your bank account. But you still owe and pay interest on the full $10,000.

Upstart's origination fees range from 0% to 12%. We saw cases with $0 fees (especially through credit union partners), but many borrowers report fees in the 5-8% range. Factor this into your decision.

How Fast Is Upstart Funding?

Blazing fast. This was the most consistent point of praise across every platform we analyzed. Over 90% of reviews mentioned how "quick" and "easy" the process was.

Most approved borrowers report getting their money in their bank account within 24 to 48 hours. For someone facing an emergency or trying to pay off a high-interest card immediately, this speed is a massive advantage over traditional banks.

5 min

Application Time

Minutes

Approval Decision

1-2 Days

Funds in Account

What Borrowers Love About Upstart

With a 4.9-star rating from over 58,000 reviews on Trustpilot, Upstart is doing something right. Here's what borrowers consistently praise:

🤖 AI-Powered Accessibility

They say "yes" when others say "no." Their AI model is a lifeline for people with fair credit who've been rejected elsewhere.

⚡ Lightning-Fast Funding

From application to money in your account in 1-2 days. The entire process is incredibly streamlined.

💰 No Prepayment Penalty

Pay your loan off early to save on interest without any extra fees. Many borrowers take advantage of this.

🔄 Repeat Customer Friendly

Many reviews are from people on their 2nd or 3rd Upstart loan, indicating strong long-term relationships.

"I just got approved for my 3rd loan after having paid off my other 2 over the course of 5 years. I am thrilled with the ease and flexibility to pay off higher interest credit cards."

— Jennifer, Trustpilot verified review, November 2026

What to Watch Out For

No lender is perfect. While the overwhelming majority of reviews are positive, there are a few common complaints:

⚠️ Common Concerns:

High APRs for Lower Credit:

If your credit is on the lower end (580-620), you could be looking at an APR over 25% or even 30%. Still better than payday loans or most credit cards, but it's steep.

Origination Fees:

Fees up to 12% can take a serious bite out of your loan. This is the price you pay for accessibility, but it adds up.

Smaller Loan Cap:

Maximum of $50,000 compared to $100,000 at SoFi or LightStream. If you need a large loan, look elsewhere.

How Does Upstart Compare to Competitors?

Think of it like this: If SoFi and Marcus are for the A+ students with 750+ credit scores, Upstart is for the B and B+ students who are smart and have potential but maybe slacked off a bit in the past. They fill a crucial gap in the market.

| Lender | APR Range | Min Credit | Max Loan | Best For |

|---|---|---|---|---|

| Upstart | 6.5%-35.99% | 580 | $50,000 | Fair credit, fast funding |

| SoFi | 8.99%-29.99% | 680 | $100,000 | Large loans, unemployment protection |

| Marcus | 6.99%-24.99% | 660 | $40,000 | No fees, competitive rates |

| LightStream | 7.49%-25.49% | 660 | $100,000 | Excellent credit, same-day funding |

The Bottom Line: Should You Use Upstart?

Here's the simple truth: If you have excellent credit (740+), you can probably get a better rate from SoFi, Marcus, or LightStream. But for the rest of us—the people with decent jobs but less-than-perfect credit histories—Upstart is a fantastic option.

They've successfully used technology to do what banks have failed to do for decades: look at a person's whole financial picture, not just a three-digit number.

✅ Consider Upstart If:

- •You have fair credit (580-680) and need a loan

- •You've been rejected by traditional lenders

- •You need money fast (1-2 days)

- •You're consolidating high-interest credit card debt

- •You have strong education/employment but weak credit history

⚠️ Shop Around If:

- •You have excellent credit (740+)

- •You need more than $50,000

- •The origination fee quote is over 8%

- •You want unemployment protection (SoFi has this)

💡 Pro Tip:

If you're consolidating credit card debt and Upstart offers you a rate that's even 5-7% lower than your cards, seriously consider it. The interest savings are real. Just be sure to factor in the origination fee—and for the love of all that is holy, don't run up your credit cards again after you pay them off!

Compare with Other Top Lenders

| Lender | APR Range | Loan Amounts | Best For | |

|---|---|---|---|---|

| Upstart | 6.5%-35.99% | $1,000-$50,000 | Fair credit, AI approval | Current Page |

| SoFi | 8.99%-29.99% | $5,000-$100,000 | Large loans, unemployment protection | Read Review → |

| Marcus | 6.99%-24.99% | $3,500-$40,000 | No fees, competitive rates | Read Review → |

| LightStream | 7.49%-25.49% | $5,000-$100,000 | Excellent credit, same-day funding | Read Review → |

| Avant | 9.95%-35.99% | $2,000-$35,000 | Bad credit, quick funding | Read Review → |